Feb 17, 2026

The report “Vacuum Insulation Panel Market By Core Material (Silica, Fiberglass, Fumed Silica, Perlite, Others), By Panel Type (Flat Panels, Special Shape Panels), By Application (Construction, Cold Chain & Logistics, Refrigeration & Freezers, Appliances, Automotive, Others) and By End-Use Industry (Residential, Commercial, Industrial)” is expected to reach USD 22.40 billion by 2033, registering a CAGR of 10.70% from 2026 to 2033, according to a new report by Transpire Insight.

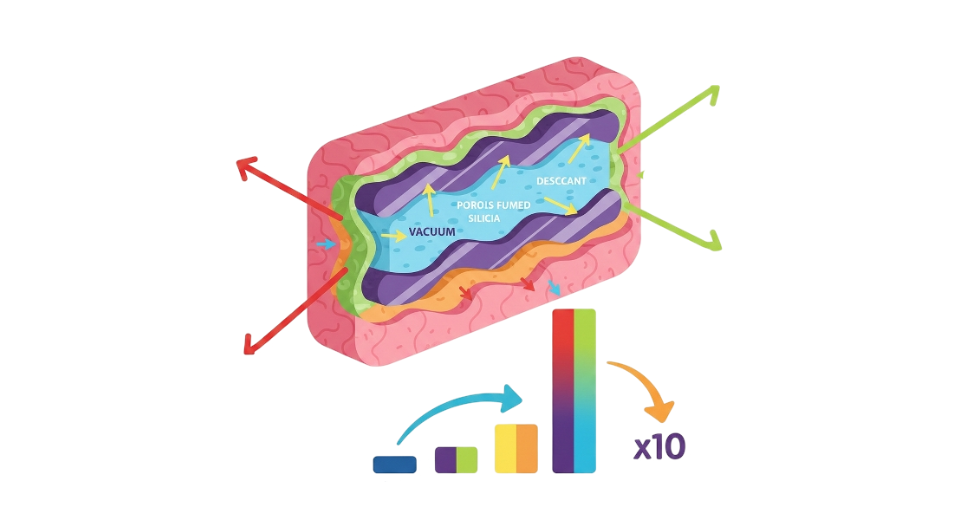

The vacuum insulation panel market is observed to be growing steadily, with industries increasingly focusing on energy efficiency and space optimization for thermal insulation. Vacuum insulation panels provide a low level of thermal conductivity, which is significantly lower compared to other conventional insulation materials. This allows for better insulation with less material thickness. This property of vacuum insulation panels is highly beneficial for industries such as construction, refrigeration, and appliance manufacturing, where energy efficiency and space optimization are critical factors for their operations. The rising awareness of energy conservation and sustainability is also adding to the growth of the vacuum insulation panel market.

The demand for these vacuum insulation panels is also being driven by the strict energy regulations and building codes that govern the construction industry. Governments and other governing bodies are encouraging the adoption of advanced insulation technologies to minimize energy consumption and carbon footprint, which will further drive the market for these products. Moreover, manufacturers are focusing on developing advanced technologies to improve the lifespan and cost-effectiveness of these products, which will further drive the market for these products and enhance their scope of applications. Another major factor that is influencing the market demand is the increase in the infrastructure of the cold chain globally. This has resulted in an increase in the movement of temperature-sensitive products, which has further fueled the need for insulation solutions that can provide internal temperature stability over long periods of time. Vacuum insulation panels provide extended internal temperature retention, which has fueled their requirement. This has further strengthened the market demand for vacuum insulation panels.

Technological advancements and the increase in the usage of vacuum insulation panels in the automotive sector are also responsible for the increase in the market demand. The rise of electric vehicles and the need for efficient thermal management systems have encouraged manufacturers to make use of high-end technology, which has fueled the growth of the vacuum insulation panel market.

The Silica segment is projected to witness the highest CAGR in the Vacuum Insulation Panel during the forecast period.

According to Transpire Insight, The silica core material segment is the dominant segment in the vacuum insulation panel market because of the high level of insulation efficiency and stability in performance over time. The silica core material provides the lowest level of thermal conductivity with the ability to withstand the test of time and environmental changes, making it ideal for construction and refrigeration purposes. The high level of stability and efficiency in the silica core material makes it ideal for meeting the insulation requirements of the construction and refrigeration industries.

In addition, the silica core material is ideal for meeting the energy efficiency regulations, making it the dominant segment in the vacuum insulation panel market. The silica core material is the preferred choice in the production of vacuum insulation panels because it provides the right balance between efficiency and stability in performance over time. The high level of efficiency and stability in the silica core material makes it ideal for meeting the insulation requirements in the construction and refrigeration industries, making it the dominant segment in the market.

The Flat Panels segment is projected to witness the highest CAGR in the Vacuum Insulation Panel during the forecast period.

The flat panels hold the highest market share within this category of panels due to their standardized design and suitability for large-scale manufacturing processes. The standardized design of flat panels allows for easier installation and incorporation into building structures, refrigeration units, and other appliances. The standardized design of flat panels minimizes manufacturing complexities and installation time, thereby making them more attractive from an economic point of view, especially when large-scale operations require uniform performance in terms of thermal performance.

Furthermore, flat panels allow for cost savings while retaining their performance and reliability as insulators for a broad array of applications. Their suitability for modular design and building appliances further solidifies their adoption, especially within commercial and residential infrastructure. As industries seek to improve their insulation capabilities while meeting regulatory requirements for energy efficiency, flat panels continue to enjoy an increased rate of demand.

The Construction segment is projected to witness the highest CAGR in the Vacuum Insulation Panel during the forecast period.

According to Transpire Insight, The construction segment is the dominant segment in the vacuum insulation panel market, and the focus on sustainable construction and energy efficiency in buildings across the globe is only increasing in importance. This is because the vacuum insulation panel provides the architect or builder with the opportunity to provide high insulation performance without compromising interior space, which is critical in the construction environment.

Moreover, the construction segment also benefits from the long-term cost savings that result from the improved efficiency in the use of heating and cooling systems in buildings. This makes the case stronger for the adoption of vacuum insulation panels, and with the increasing pace of urbanization and construction activities across the globe, the construction segment is likely to remain the dominant segment in the market.

The Commercial segment is projected to witness the highest CAGR in the Vacuum Insulation Panel during the forecast period.

The commercial end-use segment accounts for the largest market share due to increasing investments in energy-efficient infrastructure and cold storage space. Commercial buildings, including offices and retail spaces, require proper insulation to reduce energy consumption and maintain temperature stability. Vacuum insulation panels play a vital role in enhancing operational efficiency and enabling businesses to attain sustainability targets and regulations.

In addition, the focus on optimizing costs and sustainability in the long term for commercial buildings creates a market for these products. The increasing growth in organized retail and cold storage infrastructure contributes to the market demand for vacuum insulation panels in this segment, making it the market leader.

The North America region is projected to witness the highest CAGR in the Vacuum Insulation Panel during the forecast period.

North America is one of the most mature markets for Vacuum Insulation Panel, with high industrial standards, commercial construction, and regulatory requirements. The United States is the major contributor to the region's revenue generation, with strong industrial, warehousing, and healthcare sectors requiring high-quality flooring solutions. Similarly, Canada and Mexico also play their roles in the North American region, focusing on industrial upgrades, warehousing, and commercial renovation projects.

The North American region has a strong market for epoxy, polyurethane, and self-leveling flooring systems, which are increasingly being used due to their long lifespan, high chemical resistance, and low maintenance requirements. Flooring renovation projects are also adding to the growth of the Vacuum Insulation Panel industry, particularly for rapid-curing and low-VOC systems. The region also focuses on safety, hygiene, and operational efficiency, especially for industries such as food processing, pharmaceutical, and automotive. Technological advancements, along with an established contractor base and availability of high-quality resin flooring solutions, make North America one of the most prominent markets for Vacuum Insulation Panel.

Key Players

The top 15 players in the Vacuum Insulation Panel market include Panasonic Corporation, Kingspan Group plc, va-Q-tec AG, LG Hausys Ltd., Porextherm Dämmstoffe GmbH, Knauf Insulation, Etex Group, Mitsubishi Gas Chemical Company, Inc., Sekisui Chemical Co., Ltd., Owens Corning, Armacell International S.A., Vaku-Isotherm GmbH, Recticel Group, Fujian SuperTech Advanced Material Co., Ltd., and ThermoCor Inc.

Drop us an email at:

Call us on:

+91 7666513636

inquiry@transpireinsight.com

inquiry@transpireinsight.com

APAC:+91 7666513636

APAC:+91 7666513636

Address

Address