Jan 21, 2026

The report “Carbon Capture and Storage Market By Capture Technology (Post combustion, Industrial Process, Pre-combustion, Oxy-Combustion), By Application (Power generation, Oil & Gas, Metal production, Cement, Others)” is expected to reach USD 21.3 billion by 2033, registering a CAGR of 16.10% from 2026 to 2033, according to a new report by Transpire Insight.

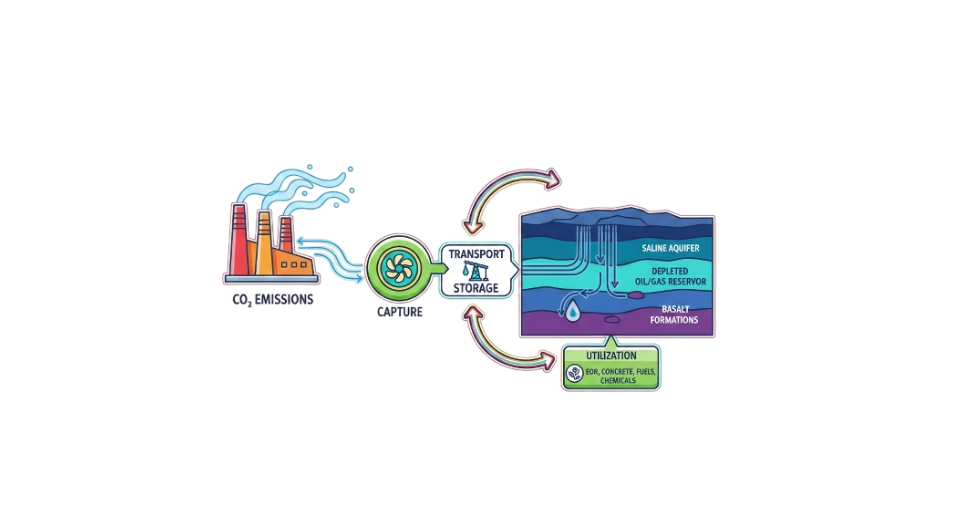

The Carbon Capture and Storage market is growing very strongly globally, with many industries and power generation segments seeking stringent climate goals and ways to reduce carbon emissions. The major use of CCS technologies has been the capturing of CO? from power plants, industrial processes, and oil and gas operations, which in turn could enable large-scale mitigation of greenhouse gases. Governments all over the world are giving their support for CCS by the way of tax incentives, emission reduction mandates, and research funding, thus giving a favorable environment for the growth of the market. Increasing energy demand and industrialization, especially in developing nations, have refocused attention on sustainable practices. Power generation is still the biggest application segment because fossil fuel-based plants remain a reality and existing plants require retrofitting to accommodate post-combustion and oxy-combustion systems, among others. The oil and gas industry also aims to deploy CCS to improve oil recovery while simultaneously lowering carbon intensity; thus, providing environmental and economic co-benefits.

The development of more advanced technologies in polymer processing and grade has enlarged the PPS applicability scope to more complex and precision-driven componentry. The emphasis of the current era on dimensional stability, better flow characteristics, and reinforcement-based formulations is mainly aimed at answering the latest performance demands. Such developments are enabling deeper PPS penetration into mature and emerging industrial applications. Advances in the use of technology in the process of polymer materials or grades are widening the use of PPS in more complex components. Companies are also developing better flow properties, filled materials, or stable dimensional components to fit required specifications. Innovative materials or grades will aid the deeper penetration of PPS into current as well as new applications.

The Post combustion segment is projected to witness the highest CAGR in the Carbon Capture and Storage market during the forecast period.

According to Transpire Insight, Post-combustion capture currently leads in the CCS technology market because it can easily be applied to already established fossil fuel-based power generation facilities. This technology provides a mechanism to selectively separate CO? from flue gas streams. This indicates that it is a relatively less disruptive technology when it comes to running the power generation facilities. This makes it an economically feasible option too. Massive projects like Shell’s Quest CCS Project in Canada have proved the viability of post-combustion capture technology.

The market benefits by incorporating improvements in solvents, sorbents, and membranes, making the capture process more efficient and decreasing energy usage. Government policies, carbon pricing, and emission policies drive the market. Post-combustion systems can be applied in regions that already have an energy production setup, as they cannot afford new power plants. This complementary ability of the technology for various applications makes it the market-leader preferred choice for carbon footprint reduction solutions in power and industrial applications.

The Power generation segment is projected to witness the highest CAGR in the Carbon Capture and Storage market during the forecast period.

The power generation segment currently leads due to the use of coal-, gas-, and biomass-fueled power generation worldwide. The power generation process is a major contributor of carbon dioxide emissions in the environment; hence, these power generation facilities are ideal targets for applying CCS. The post-combustion and oxy-combustion methods are being employed in retrofitted and new power generation facilities, which result in reduced carbon dioxide emissions without reducing power generation efficiency.

Further support for the market is provided by various government-backed programs, subsidies, and climate policies that promote the widespread use of CCS technology within the energy production industry. Advances in monitoring capabilities, ensuring integration with renewable energy resources, and even generating new revenue streams via EOR or CO2 utilization offer important drivers for this market as well. CCS technology is characterized by the use of power plants that act as an intermediary between the use of fossil fuels and renewable energy resources for the production of energy.

The North America region is projected to witness the highest CAGR in the Carbon Capture and Storage market during the forecast period.

The largest market for CCS is in North America, and it is largely driven by the United States and Canadian emphasis on cutting emissions in industrial and power sectors. The area has well-developed infrastructure to transport and store CO2, and thus large-scale implementation of CCS projects is being carried out. Government support, tax credits, and joint ventures have further encouraged spending, especially to retro-engineer existing coal and gas-based power plants by post-combustion and oxygen combustion methods. Technical and economically feasible implementation of CCS solutions has been proven by various projects, such as Quest in Canada and various pilot projects in the United States, and thus it dominates other regions in international market trends. The regional demand is fueled by factors such as various regulatory policies, sustainable initiatives from the energy and industry sectors, and continuing research and development in carbon capture, transport, and storage technology. In North America, there is also a lead in the integration of CCS with Enhanced Oil Recovery, thus providing economic as well as environmentally favorable advantages. The presence of experience in the development of technological solutions and in-large-scale project development, together with access to innovative financing solutions, makes North America a leading region in CCS development, with a future that could extend to further applications in different industries and integrating with new low-carbon technologies.

Key Players

The top 15 players in the Carbon Capture and Storage market include Royal Dutch Shell plc, ExxonMobil Corporation, Chevron Corporation, Equinor ASA, TotalEnergies SE, Aker Solutions ASA, Mitsubishi Heavy Industries Ltd., Siemens Energy AG, Fluor Corporation, Linde plc, Halliburton Company, Baker Hughes Company, Schlumberger Limited, Sulzer Ltd., and Carbon Engineering Ltd.

Drop us an email at:

Call us on:

+91 7666513636

inquiry@transpireinsight.com

inquiry@transpireinsight.com

APAC:+91 7666513636

APAC:+91 7666513636

Address

Address