Jan 09, 2026

The report “Antibody Drug Conjugates (ADCs) market By Product (Kadcyla, Enhertu, Adcetris, Padcev, Trodelvy, Polivy, and others), By Disease Type (Breast Cancer, Blood Cancer, others), By Linker Type (Non-Cleavable, Cleavable), By Target (HER2, CD22, CD30, Others) By Payload Type (MMAE/auristain, Calicheamicin, Maytansinoids, Others)” is expected to reach USD 32.19 billion by 2033, registering a CAGR of 10.50% from 2026 to 2033, according to a new report by Transpire Insight.

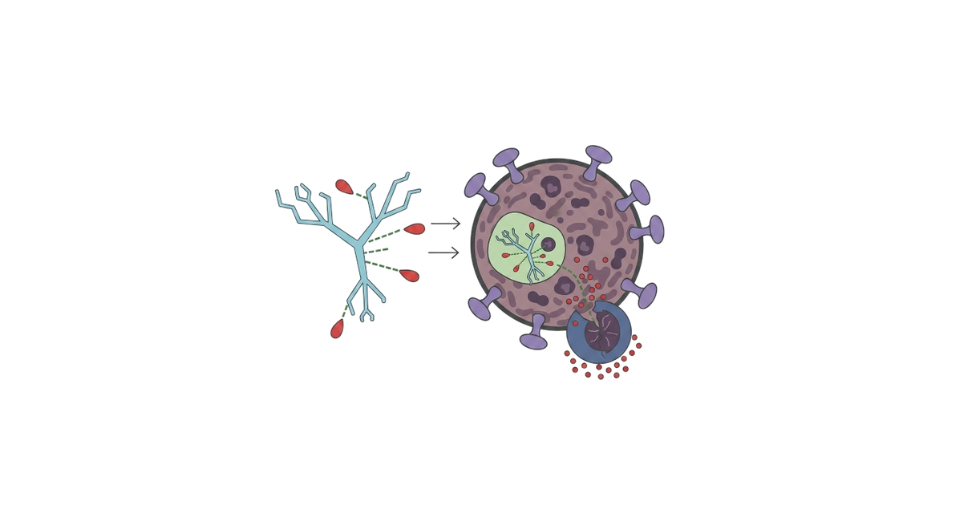

The Antibody Drug Conjugates (ADCs) market is revolutionizing the world of cancer therapy by shifting focus from traditional chemotherapy to highly targeted and data-informed cancer therapies. ADCs are designed to target cancer by conjugating a monoclonal antibody, cytotoxic drug, and sophisticated linker technologies to provide targeted delivery of a highly potent drug to cancer cells. The targeted mode of action of ADCs has made it possible to specifically kill cancer cells with minimal damage to normal tissues. The increased focus on biomarker-based therapies and enhanced expertise in antibody, linker, and cytotoxic drug technologies is making it possible to monitor cancer progression and manage it more effectively. The ADCs industry is primarily driven by the growing incidence of cancers worldwide, the pursuit for more effective therapies with fewer side effects, and the mounting momentum for personalized cancer treatment options. The rising understanding for personalized medicine issues and the necessity for combatting drug-resistant cancers have propelled the adoption of ADCs. Moreover, the rising understanding for personalized medicine issues and the necessity for combating drug-resistant cancers have propelled the adoption of ADCs. Additionally, developments in clinical trial data analytics, AI-driven drug development, and streamlined manufacturing platforms are making it feasible for pharmaceutical companies to develop and optimize ADCs with improved safety and shorter time-to-market launches. From a regional perspective, mature markets like North America and Europe have high ADC adoption on account of a strong healthcare infrastructure, deep oncology research activity, and favorable regulatory landscapes that support innovative cancer treatments. Therefore, Asia Pacific emerges as a high-growth region, driven by the growing incidence of cancer, increasing access to state-of-the-art treatments, governmental support for innovation in biopharmaceuticals, and value-friendly clinical development capabilities. This growing global footprint is allowing access to ADC therapies to a broader patient population and is positioning the ADC market as a critical pillar in the future of targeted cancer treatment.

The Kadcyla segment is projected to witness the highest CAGR in the Antibody Drug Conjugates (ADCs) market during the forecast period.

According to Transpire Insight, Kadcyla has remained one of the most established and commercially successful products in the Antibody Drug Conjugate (ADCs) market and has remained the benchmark for ADC technology. It was among the first products to demonstrate that combining a targeted monoclonal antibody with a cytotoxic payload could provide clinical benefit with reduced systemic toxicity relative to chemotherapy. The longevity of experience in the market has helped validate ADCs as an established and scalable class of products for treating cancers in patients.

The Breast Cancer segment is projected to witness the highest CAGR in the Antibody Drug Conjugates (ADCs) market during the forecast period.

The major segments present in the Cancer Cytotoxic Drug Market are Breast Cancer, followed by blood cancers. However, the remaining solid tumors make up another stable segment.

The largest market share for the ADC market is held by the Breast Cancer market, and the main reason is that the breast cancer market is the oldest and most successful therapeutic market to evolve and capitalize on ADC technology to date. The large prevalence of breast cancer alongside clearly identifiable targets and clinical validation in humans is the primary reason for the overall adoption of ADCs in the breast cancer market.

The Cleavable segment is projected to witness the highest CAGR in the Antibody Drug Conjugates (ADCs) market during the forecast period.

According to Transpire Insight, Cleavable linkers are the dominant ones because they have the ability to release the cytotoxic agent in accordance with the conditions that exist within the cancerous cells. Due to this capability, the linker is able to produce enhanced killing of the tumor cells, have enhanced potency, and be effective in the treatment of both solid cancers and blood cancers. Its capability to bring forth the “bystander effect” is also a significant advantage.

The HER2 segment is projected to witness the highest CAGR in the Antibody Drug Conjugates (ADCs) market during the forecast period.

HER2 is the leading target its overexpression occurs frequently in breast cancers and gastric cancers, which comprise the largest patient base targeted with ADC therapies. The success of HER2-targeting ADCs as a treatment modality has already established a precedent for effectiveness, safety, and market feasibility, making HER2 the gold standard for targets within the market. Additionally, there are already diagnostic methods available for its expression.

The North America region is projected to witness the highest CAGR in the Antibody Drug Conjugates (ADCs) market during the forecast period.

The most prominent area among these regions is North America, with its highly developed infrastructure for healthcare, along with high prevalence rates for cancer. The country also houses some of the biggest pharma companies with considerable knowledge and know-how regarding ADCs. In fact, most ADCs are commercialized rapidly because they are developed by companies with considerable technological knowledge regarding ADCs. The high prevalence rate for cancer, specifically breast cancer as well as blood cancer, also boosts demand for more targeted drugs with fewer adverse reactions. The developed clinical infrastructure for precision medicine also fosters rapid growth for commercializing new drugs, with highly developed pathways for clinicians at Health Canada as well as FDA for drug approval. The high expenditure for healthcare also encourages clinicians to opt for high-cost drugs, making this region witness the maximum growth for ADCs. In fact, this region remains the biggest for ADCs currently.

Key Players

The top players in the Antibody Drug Conjugates (ADCs) market include Seagen, Inc., Takeda Pharmaceutical Company Ltd., AstraZeneca, F. Hoffmann-La Roche Ltd., Pfizer, Inc., Gilead Sciences, Inc., Daiichi Sankyo Company Ltd., and antibody drug conjugates Therapeutics SA.

Drop us an email at:

Call us on:

+91 7666513636

inquiry@transpireinsight.com

inquiry@transpireinsight.com

APAC:+91 7666513636

APAC:+91 7666513636

Address

Address