Europe Aerospace Composite Market Size & Forecast:

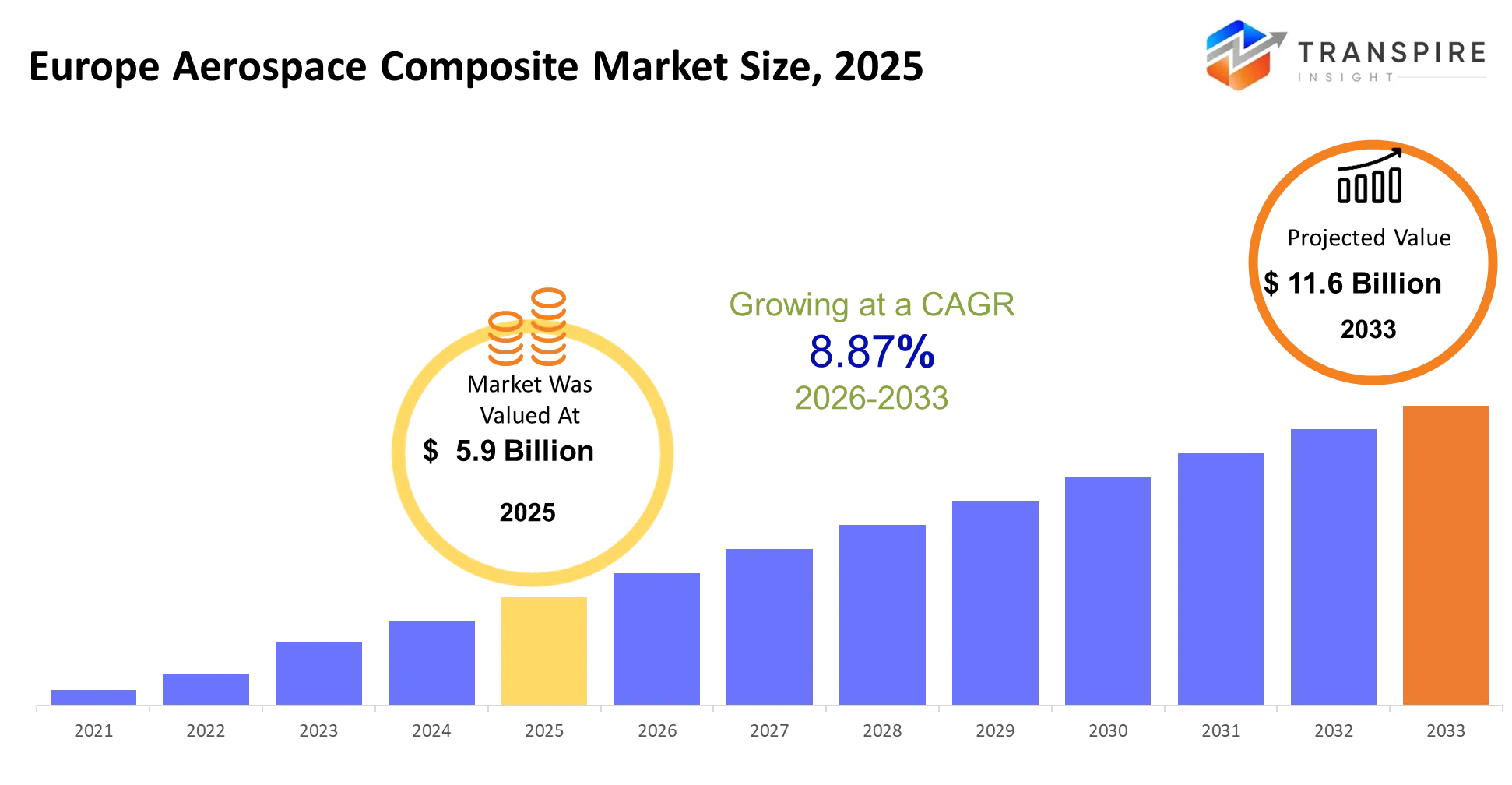

- Europe Aerospace Composite Market Size 2025: USD 5.9 Billion

- Europe Aerospace Composite Market Size 2033: USD 11.6 Billion

- Europe Aerospace Composite Market CAGR: 8.87%

- Europe Aerospace Composite Market Segments: By Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Others); By Application (Aircraft Structures, Interiors, Engines, Spacecraft, Others); By End-User (Aerospace OEMs, Defense Sector, Airlines, Space Agencies, Others); By Resin (Epoxy, Polyester, Thermoplastic, Others)

To learn more about this report,  Download Free Sample Report

Download Free Sample Report

Europe Aerospace Composite Market Summary

The Europe Aerospace Composite Market was valued at USD 5.9 Billion in 2025. It is forecast to reach USD 11.6 Billion by 2033. That is a CAGR of 8.87% over the period.

The Europe aerospace composite market supplies lightweight, high-strength materials that help aircraft fly farther on less fuel while maintaining structural integrity and safety. The use of these composites enables airlines and manufacturers to replace heavier metals which exist in fuselages and wings and interiors thus achieving operational cost reductions and fulfilling their stringent emissions requirements.

Automation through fiber placement technology together with digital manufacturing systems established new production methods which enhanced product quality while decreasing operational waste. The tighter Europeans emission regulations together with their net zero commitments served as the main external factor which forced OEMs to speed up their composite material development for upcoming aircraft platforms.

The combination of these elements has led to changes in both procurement processes and design standards. The connection between fuel efficiency and operational profitability which drives compliance requirements has led manufacturers to use composite materials in their mid-range aircraft production after starting with their main aircraft products. The aerospace industry now experiences a transformation which results in extended supply contracts that deliver increased material quantities while organizations throughout the value chain engage in more substantial partnerships.

Key Market Insights

- The Europe Aerospace Composite Market in 2024 is primarily controlled by Western Europe which holds more than 65% market share because of its strong base of original equipment manufacturers.

- The demand for aerospace products in this region is led by Germany and France and the UK which benefit from their aerospace manufacturing centers and government-funded research and development projects.

- The region of Eastern Europe will experience its highest growth rate until 2030 because of its ability to produce goods at low expenses while its supplier network continues to expand.

- Carbon fiber composites will control the market with more than 55% share in 2024 because they deliver superior strength-to-weight performance which makes them suitable for all aircraft structural needs.

- The market for glass fiber composites operates as the second biggest segment because customers prefer the material which provides budget-friendly options for making secondary parts of aircraft.

- The market for ceramic matrix composites will experience its fastest growth between now and 2030 because of their increasing use in high-temperature engine parts and defense systems.

- Airlines maintain their focus on lightweight materials which help them achieve fuel savings and emissions reductions thus making commercial aviation the largest market with approximately 60% share.

- The defense aviation sector experiences its strongest growth because military budgets increase and advanced lightweight materials become essential for defense purposes.

- The Europe Aerospace Composite Market is controlled by aircraft manufacturers who hold more than 70% market share because they have established original equipment manufacturer relationships to develop new aircraft systems.

- The production process in companies benefits from automation technologies which include fiber placement and digital manufacturing because these technologies help organizations expand their manufacturing output while maintaining product quality and decreasing material waste.

What are the Key Drivers, Restraints, and Opportunities in the Europe Aerospace Composite Market?

Driver:

The European Aerospace Composite Market experiences growth because European aviation emissions standards have become stricter through European Commission climate targets. Aircraft manufacturers face direct financial pressure to reduce fuel burn which pushes them to replace aluminum with carbon fiber composites in primary structures. The shift requires total change. The Airbus programs now use composite materials for more extensive aircraft components which results in greater material requirements per aircraft. Composite suppliers achieve increased revenue per unit through their long-term supply agreements which depend on production supply shortages.

Restraint:

The industry faces two main challenges because of high production costs and certification expenses which create permanent obstacles. Composite manufacturing requires specialized tooling equipment and autoclaves together with skilled labor which incurs high initial setup costs. The aerospace certification process requires extensive time because it needs multiple years to get new material approvals. The process creates two main problems because it delays product launch and makes it hard to replace old airplane systems. The result suppresses immediate revenue growth for smaller suppliers who lack either funding to grow their business or ability to handle regulatory challenges.

Opportunity:

The market shows potential for growth through the development of thermoplastic composites which will be manufactured using automated processes. The automated fiber placement technology enables manufacturers to produce their products at faster rates while decreasing production time requirements. The digital manufacturing hubs in Germany and France are being established as demonstration sites for this advanced manufacturing technology. The processes establish cost efficiencies which enable composite materials to be used in high-volume aircraft manufacturing resulting in increased usage for both commercial and defense aviation.

What Has the Impact of Artificial Intelligence Been on the Europe Aerospace Composite Market?

European aerospace composite design production and maintenance practices undergo transformation through the implementation of artificial intelligence and advanced digital technologies. Manufacturers utilize AI-based control systems to automate the processes of fiber placement and resin infusion and curing, which results in higher accuracy and decreased material waste. The system performs constant monitoring of temperature and pressure and layup accuracy to enable real-time modifications that improve production efficiency and decrease product flaws. Machine learning models utilize historical performance data to predict material fatigue patterns which enable maintenance to occur earlier and prolong the lifespan of components. The results of this process have achieved specific results which demonstrate an reduction in aircraft downtime and a decrease in lifecycle maintenance costs for fleets that heavily use composite materials.

Digital twins are experiencing an increase in popularity among OEMs who use virtual models to test structural behavior under various stress conditions. The engineers can determine optimal composite usage through digital twin technology which enables them to complete their design work before physical production starts, thus reducing development time while enhancing fuel efficiency. The system still has one major restriction that needs to be addressed. AI adoption requires high-quality, standardized datasets across the value chain, which remain fragmented due to proprietary systems and varying certification requirements. The real-world aerospace manufacturing environments experience operational delays because of this issue, which prevents them from achieving complete AI-driven optimization through system integration.

Key Market Trends

- Airbus and other original equipment manufacturers have raised their usage of composite materials in new aircraft designs since 2020 while they establish new design standards which focus on creating lightweight structures that minimize fuel consumption.

- European authorities established stricter emission regulations between 2021 and 2024 which required manufacturers to speed up their transition from aluminum materials to high-performance carbon fiber composites.

- The adoption of automated fiber placement technology spread to all major industrial centers after 2022 because it helped aircraft manufacturers achieve better production results through reduced material waste and standardized manufacturing processes.

- Since 2022 supply chains have developed regional patterns because manufacturers now obtain materials from Eastern European countries to lessen their reliance on worldwide composite material shipments.

- The adoption of thermoplastic composites increased after 2023 because manufacturers needed materials which could be processed more quickly and had better recyclability for their upcoming aircraft development projects.

- The European defense budget increases since 2021 have created more demand for military aircraft which use composite materials that can withstand extreme temperatures and high impacts.

- Tier-1 suppliers have moved toward long-term contracts and risk-sharing agreements with OEMs, which now provide them stable income from contracts while protecting material access through supply agreements.

- Digital twin technology became more popular after 2022 because it enables engineers to create composite performance simulations which reduce development time and decrease design testing expenses.

- The European Union has established sustainability reporting rules since 2023 which require companies to develop recyclable composite materials and implement circular production methods.

Europe Aerospace Composite Market Segmentation

By Type:

Carbon fiber composites maintain their market dominance because they account for over 50 percent of total material consumption. Aircraft manufacturers use carbon fiber material for their fuselage and wing construction because this material delivers better flight performance which reduces their operational costs. Glass fiber composites maintain the second-largest market share because they provide an economical solution for secondary components which do not require extreme strength protection. Aramid fiber composites serve niche applications that require high impact resistance and fatigue tolerance, particularly in defense and rotorcraft segments.

The demand for carbon fiber materials increases because next-generation aircraft programs require more carbon fiber usage. The demand for glass fiber remains constant because its applications target cost-sensitive markets.

The future market demand will support hybrid material systems that combine carbon and thermoplastics. This growth will require suppliers to develop solutions for integrating multiple materials together. Investors and manufacturers will likely focus on improving production efficiency and reducing raw material costs to expand adoption across mid-range aircraft platforms.

By Application:

Aircraft structures represent the primary use of composite materials because their construction requires extensive composite integration for wings and fuselage sections and load-bearing components. Structural applications need high-performance materials which provide durability and weight reduction together with protection against environmental stress. The interior space of an aircraft represents the second-largest segment which requires lightweight cabin components. This requirement enables increased passenger capacity while also decreasing fuel consumption.Engine and spacecraft applications present smaller operational scope yet maintain critical technical value because they operate under extreme environmental conditions.

Structural applications experience growth from the current aircraft development cycles, whereas interior applications develop at a steady pace as airlines modernize their aircraft fleets to enhance operational efficiency and improve customer satisfaction. Engine composites experience growing popularity because advanced propulsion systems require more heat-resistant materials to meet rising demand.

Future trends predict that composite materials will extend their use into aircraft engines and space vehicle designs through new material development. Product developers will target high-temperature performance testing and certification readiness functions to seize business opportunities in developing advanced aerospace systems.

By End-User:

The aerospace Original Equipment Manufacturer market leads the market because aerospace companies directly use composite materials to build their aircraft. The major manufacturers experience stable product demand because their businesses have strong order backlogs and extended production times. The defense sector represents a significant secondary segment, supported by increasing military investments in lightweight and high-strength materials for advanced aircraft. Airlines contribute to the economy because they need retrofitting and their operations need better efficiency.

The demand for Original Equipment Manufacturers increases because aircraft innovation continues, while defense requirements expand because of modernization efforts and geopolitical conflicts. Space agencies remain a smaller but high-value segment, focusing on specialized composite applications for satellites and launch vehicles.

Future growth will see defense and space segments expand at a faster pace because of technological advancements and government funding. Suppliers and investors will target high-performance materials and long-term contracts with OEMs and defense organizations to secure stable revenue streams.

By Resin:

The market exists because epoxy resins provide both strong mechanical properties and chemical resistance together with their established use in aerospace structural components. The market share of polyester resins remains limited because they only serve non-critical applications that prioritize cost savings above performance needs. Manufacturers show increasing interest in thermoplastic resins because these materials enable quicker production times together with their capacity for recycling in manufacturing processes.

The growth of epoxy products maintains steady progress because their performance remains trustworthy across all aircraft programs which have obtained certification. Thermoplastics demonstrate greater growth because they enable shorter manufacturing cycles which work well with automated production methods. The use of polyester materials in aerospace applications remains restricted because these materials do not meet performance standards required for challenging aerospace environments.

Thermoplastic systems will become more important because companies will prioritize production scalability together with environmentally friendly practices. Material suppliers will create new business possibilities through their investment in advanced resin formulations which provide performance and cost advantages while minimizing environmental impact across multiple aerospace manufacturing projects.

What are the Key Use Cases Driving the Europe Aerospace Composite Market?

Aircraft primary structures represent the core use case, where composites replace aluminum in fuselage sections and wings to cut weight and fuel burn. The materials used by manufacturers such as Airbus enable them to achieve European emissions standards while reducing operating costs during long-distance flights.

Defense aircraft components and cabin interiors are developing new application areas. Airlines use lightweight composite seating and panels to improve payload capacity, while defense programs implement impact-resistant materials in their rotorcraft and fighter jets to boost durability and operational effectiveness.

The development of new applications has created demand for high-temperature engine components and spacecraft structures. Thermoplastic composites and ceramic matrix materials demonstrate excellent capabilities for use in propulsion systems and satellite platforms which require heat resistance and structural stability to advance next-generation aerospace development.

|

Report Metrics |

Details |

|

Market size value in 2025 |

USD 5.9 Billion |

|

Market size value in 2026 |

USD 6.4 Billion |

|

Revenue forecast in 2033 |

USD 11.6 Billion |

|

Growth rate |

CAGR of 8.87% from 2026 to 2033 |

|

Base year |

2025 |

|

Historical data |

2021 - 2024 |

|

Forecast period |

2026 - 2033 |

|

Report coverage |

Revenue forecast, competitive landscape, growth factors, and trends |

|

Regional scope |

Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe) |

|

Key company profiled |

Hexcel, Toray, Solvay, Teijin, Mitsubishi Chemical, SGL Carbon, Owens Corning, Gurit, BASF, Dow, Huntsman, Cytec, Axiom Materials, TenCate, Park Aerospace |

|

Customization scope |

Free report customization (country, regional & segment scope). Avail customized purchase options to meet your exact research needs. |

|

Report Segmentation |

By Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Others); By Application (Aircraft Structures, Interiors, Engines, Spacecraft, Others); By End-User (Aerospace OEMs, Defense Sector, Airlines, Space Agencies, Others); By Resin (Epoxy, Polyester, Thermoplastic, Others) |

Which Regions are Driving the Europe Aerospace Composite Market Growth?

The aerospace manufacturing sector in Western Europe together with its compliance to European Commission climate targets shows that Western Europe leads all other regions. The countries of Germany France and the United Kingdom serve as bases for essential OEMs and Tier-1 suppliers and research clusters that drive ongoing development of composite materials. The established certification systems together with complete supplier integration enable organizations to quickly implement new materials into their aircraft development projects. The existing system of universities and testing centers and government funding creates a reliable system that advances development of high-performance composite materials.

Southern Europe maintains its second position through its continuous investment in aerospace and its expanding network of mid-sized aerospace suppliers. The countries of Italy and Spain concentrate on producing components and assembling them instead of creating complete aircraft. The region achieves cost advantages through reduced labor expenses while still meeting European aerospace industry requirements. The ongoing participation in international aircraft development projects creates a stable demand pattern which helps maintain sustainable revenue growth.

Eastern Europe has achieved its highest growth rate because of its new investments which support economical production methods and help companies develop their supply networks. Since 2022 Poland and Romaniahave established new aerospace industrial parks which have successfully drawn international direct investment. Western original equipment manufacturers (OEMs) have moved some of their operations to the الشرق because of the region's lower production expenses and its availability of highly qualified workforce. The present momentum establishes business opportunities for new suppliers and investors who plan to grow their businesses between 2026 and 2033.

Who are the Key Players in the Europe Aerospace Composite Market and How Do They Compete?

The European aerospace composite industry currently sees its competitive landscape approximately divided between major material science companies and their related original equipment manufacturer partners, who deliver high-value contracts. The established companies maintain their market share by using their unique product formulas and extensive certification capabilities and their ongoing contracts with aircraft manufacturers. The primary method of competition depends on technological advancements, while high-performance carbon fiber systems and automated manufacturing capabilities function as the most important competitive differentiators. The aerospace industry certification requirements create barriers that prevent new companies from entering core aerospace programs, but smaller companies have found success in developing thermoplastic and recycling-based solutions for specialized markets

Toray Industries establishes its leadership position through its advanced carbon fiber and prepreg systems, which provide complete supply chain solutions to European OEM manufacturers. The company establishes its unique position through its ability to deliver consistent fiber quality and maintain production capabilities, which enable it to support high-demand military aircraft manufacturing requirements. Solvay develops advanced thermoset and thermoplastic composite materials, which it uses to create next-generation aircraft systems, thanks to its aerospace industry certifications and close relationships with original equipment manufacturers.

SGL Carbon establishes its competitive advantage through its nearby manufacturing operations in Europe, which enable the company to create tailored composite materials for both industrial and structural needs. Teijin focuses on developing its business operations through its thermoplastics and sustainable compostable products, which the company markets as environmentally friendly because of their recyclability and quick processing capabilities. The companies establish their market presence through joint development partnerships and regional production capacity expansion and collaborative work with aerospace manufacturing systems.

Company List

- Hexcel

- Toray

- Solvay

- Teijin

- Mitsubishi Chemical

- SGL Carbon

- Owens Corning

- Gurit

- BASF

- Dow

- Huntsman

- Cytec

- Axiom Materials

- TenCate

- Park Aerospace

Recent Development News

“In March 2026, Hexcel Corporation showcased next-generation aerospace composite solutions at JEC World 2026 in Paris. The launch highlighted scalable thermoplastic materials and automated manufacturing technologies aimed at improving production efficiency and supporting high-rate aircraft programs. https://www.hexcel.com

“In March 2026, Teijin showcased new carbon fiber and thermoplastic composite solutions at JEC World 2026. These product launches focus on scalable, recyclable materials, accelerating adoption of sustainable composites in aerospace manufacturing. https://www.teijincarbon.com

What Strategic Insights Define the Future of the Europe Aerospace Composite Market?

The Europe Aerospace Composite Market is moving toward high-rate, automated production supported by thermoplastic materials and digital manufacturing. The industry requires this approach because next-generation aircraft need higher production capacity while they must achieve tighter emissions limits and lower operating costs. Narrow-body and regional aircraft will start to use composites because those aircraft need to achieve production efficiency which will support their operational needs.

The carbon fiber supply chain operates as a hidden risk because manufacturers depend on both carbon fiber production and its precursor materials. The limited number of suppliers which manufacturers can choose from will create two major risks because it will lead to price fluctuations and exporter shortages which will both cause production delays and reduce profit margins.

The European Union circular economy framework creates an emerging market opportunity for recyclable thermoplastic composites. The first investment into closed-loop recycling systems will create business opportunities which will provide companies with regulatory benefits.

Market participants should invest in production systems that combine automation with secure partnerships for raw material supply to achieve scalable operations while maintaining strong supply chain resilience.

Europe Aerospace Composite Market Report Segmentation

By Type

- Carbon Fiber Composites

- Glass Fiber Composites

- Aramid Fiber Composites

- Others

By Application

- Aircraft Structures

- Interiors

- Engines

- Spacecraft

- Others

By End-User

- Aerospace OEMs

- Defense Sector

- Airlines

- Space Agencies

- Others

By Resin

- Epoxy

- Polyester

- Thermoplastic

- Others

Frequently Asked Questions

Find quick answers to common questions.

The Europe Aerospace Composite Market size is USD 11.6 Billion in 2033.

Key segments for the Europe Aerospace Composite Market are By Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Others); By Application (Aircraft Structures, Interiors, Engines, Spacecraft, Others); By End-User (Aerospace OEMs, Defense Sector, Airlines, Space Agencies, Others); By Resin (Epoxy, Polyester, Thermoplastic, Others).

Major Europe Aerospace Composite Market players are Hexcel, Toray, Solvay, Teijin, Mitsubishi Chemical, SGL Carbon, Owens Corning, Gurit, BASF, Dow, Huntsman, Cytec, Axiom Materials, TenCate, Park Aerospace

The Europe Aerospace Composite Market size is USD 5.9 Billion in 2025.

The Europe Aerospace Composite Market CAGR is 8.87% from 2026 to 2033.

- Hexcel

- Toray

- Solvay

- Teijin

- Mitsubishi Chemical

- SGL Carbon

- Owens Corning

- Gurit

- BASF

- Dow

- Huntsman

- Cytec

- Axiom Materials

- TenCate

- Park Aerospace

Recently Published Reports

-

Apr 2026

Healthcare Polymer Packaging Market

Healthcare Polymer Packaging Market Size, Share & Analysis Report By Packaging Type (Syringes, IV Bottles and Pouches, Clamshells, Blisters, Bottles & Jars, Containers, Tubes, IV Parental Packaging, Others), By Type (Regulated, Non-regulated), By Polymer Type (LDPE (Low-Density Polyethylene), HDPE (High-Density Polyethylene), Homo-polymer (Homo), Random Copolymer (Random), Block Copolymer (Block), PET, Polystyrene, Polyvinyl Chloride, Polyamide/EVOH, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Apr 2026

Hydrophilic Tape (Waterstop) Market

Hydrophilic Tape (Waterstop) Market Size, Share & Analysis Report By Type (Bentonite-Based Hydrophilic Tape, Rubber-Based Hydrophilic Tape), By Application (Residential Buildings, Commercial Buildings, Infrastructure Projects), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Apr 2026

Metalens Market

Metalens Market Size, Share & Analysis Report By Type (Visible Light Metalens, and Infrared Metalens), By Application (Consumer Electronics, Automotive Electronics, Industrial, Medical, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Apr 2026

PBT Resin Market

PBT Resin Market Size, Share & Analysis Report By Type (Reinforced PBT Resin, Unreinforced PBT Resin), By Processing Method (Injection Molding, Extrusion, Blow Molding, Others), By End-User (Automotive, Electrical & Electronics, Consumer Appliances, Industrial Machinery, Medical Devices, Packaging, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031