Market Summary

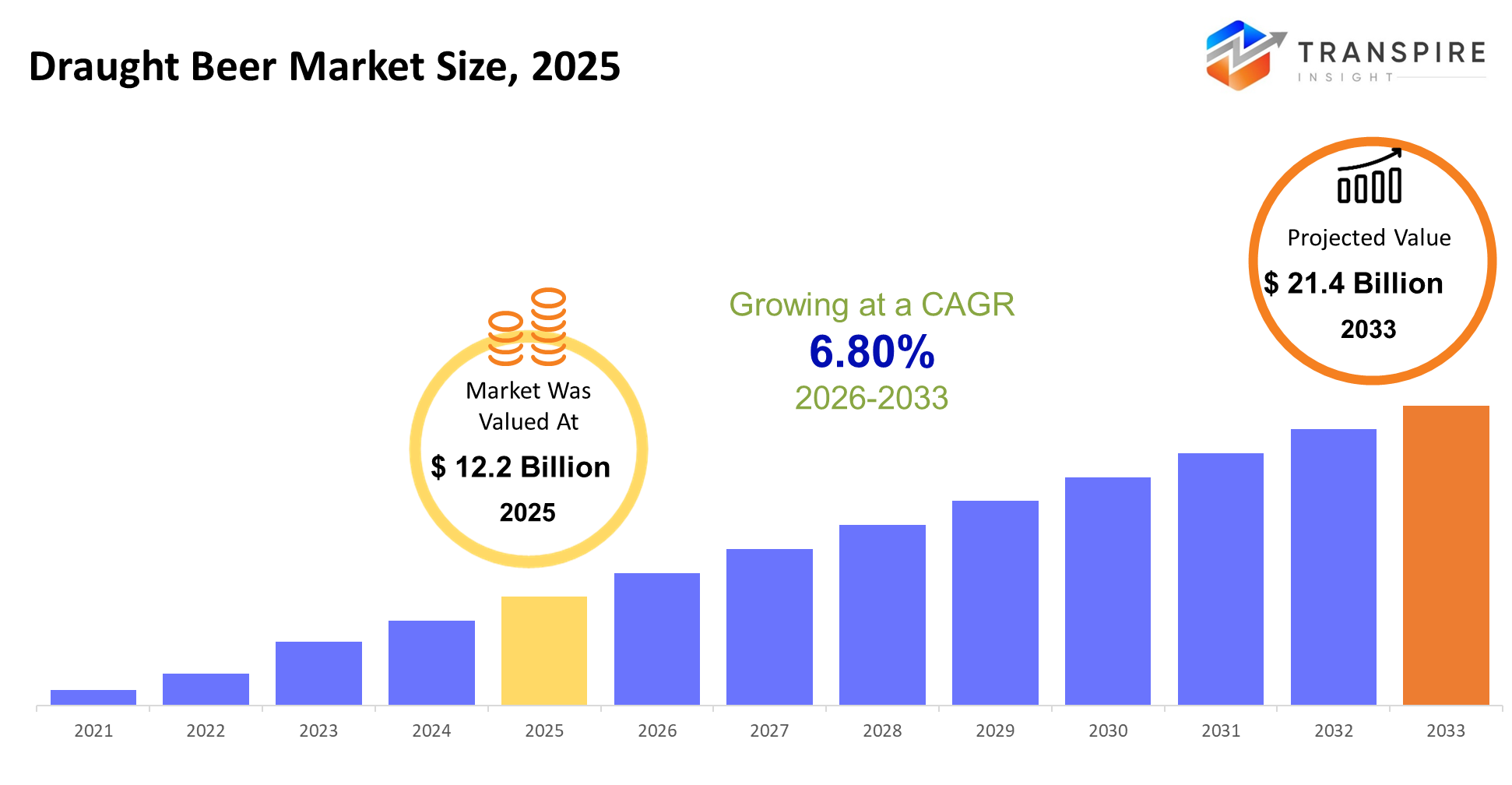

The global Draught Beer market size was valued at USD 12.2 billion in 2025 and is projected to reach USD 21.4 billion by 2033, growing at a CAGR of 6.80% from 2026 to 2033. The draught beer market is projected to grow steadily due to expanding on-trade consumption, premiumization of alcoholic beverages, and rising urban socialization trends. Growth is further supported by craft beer penetration, hospitality sector recovery and increasing investments in modern tap infrastructure across emerging and developed economies.

Market Size & Forecast

- 2025 Market Size: USD 12.2 Billion

- 2033 Projected Market Size: USD 21.4 Billion

- CAGR (2026-2033): 6.80%

- North America: Largest Market in 2026

- Asia Pacific: Fastest Growing Market

To learn more about this report,  Download Free Sample Report

Download Free Sample Report

Key Market Trends Analysis

- In North America, there is an established pub and sports bar culture, and beer consumed in draft form has long had a role in drinking social events, thanks to continuous demand from larger venues and an established craft brewing sector.

- United States: There is stronger momentum in the United States, particularly in the draught category. Consumers in the United States seek draught bars, seasonal beers, and keg beers, hence promoting higher per-capita spending in the on-trade channels.

- The Asia Pacific market has strong growth potential, thanks to the increasing adoption of draught beer spurred by urbanization, increasing disposable incomes, and the westernized nightlife culture in the region, specifically in urban settings where premium taps and foreign beer brands are gradually gaining recognition.

- Keg beer comes up as the most prominent type segment, primarily based on efficiency, shelf life, and suitability in high-volume service operations, making keg beer the preferred option for pubs, restaurants, hotels, and entertainment outlets across the world.

- Premium-class draught beer drives category-based growth as a result of consumer preference for upgrading their purchase options from regular versions to get improved flavor, brand images, as well as quality associated with premium products.

- Commercial use presently has the dominant share in the market for draught beer and is responsible for the leading share of global consumption. It assists in attracting people and generating profits in bars and pubs, as well as in hotels and stadiums to gain consumer attention in comparison to other packaging types of beer.

The Draught beer market referred to as draught beer encompasses the on-trade distribution of beer from kegs/casks via taps in pubs, restaurants, and other entertainment and eating-out venues. Unlike bottled beer, the main focus regarding beer in kegs/casks is freshness and consumer experience. Market dynamics are being propelled by factors such as the rise in consumer preference for premium beer, the rise in the number of outings, and the resultant rise in the power of the craft beer trend. Draught beer is perceived to be of better quality, which acts as an incentive for repeat business. There have also been some developments in the cold chain logistics, which have helped improve product quality. In terms of commercial viability, it can be said that for operators that conduct on-trade sales, draught beer has more revenue-generating potential than other beer types that can be purchased in bottles, thereby making it an important product segment for operations in this industry. In view of an improvement in the tourist industry, it can be noted that an increase in value has become an important trend for the draught beer industry, which was earlier experiencing growth based on volumes.

Draught Beer Market Segmentation

By Type

- Keg Beer

Keg beer leads owing to its scalable nature and ability to be handled easily. Its long life after tapping and compatibility with common dispensing systems ensure commercial viability in the on-trade retail market.

- Cask Beer

Cask beers still remain a niche but significant sector, which gets motivated by conventional brewing practices and consumer preference for natural conditioning. Such beers also tend to attract their targeted consumer base who value authenticity, particularly where conventional pubs and brews carry more significance.

To learn more about this report, Download Free Sample Report

By Category

- Super Premium

Super premium draught beer growth is driven by experiential consumption trends, craft innovation, and limited edition products. This category enjoys the benefit of the target market of affluent consumers seeking differentiation through unique taste profiles.

- Premium

High-quality beer for drafting has an appropriate level of quality and appeal, targeting a wide segment of customers. Quality, recognition, and a perception of being an upgrade for regular beer make this product sell steadily in developed and developing markets.

- Regular

This is a common form of beer that produces a high level of sales volumes as a result of its affordability and familiarity among consumers. This type of beer is currently a mainstay within the overall draft beer sales channels.

By End Use

- Commercial

Commercial establishments can also benefit from the operational efficiency, lower packaging cost per unit, and consistent quality control with keg and cask systems. Offering draught exclusives and seasonal taps increases brand differentiation and supports higher average spend per customer.

- Home

Home beer sales can be viewed under the influence of changing lifestyles, specifically for urban and wealthy households. Though constrained by storage and equipment-related expenditures, this segment can leverage experience and thus move along with overall premium liquor sales trend lines.

Regional Insights

North America, driven by the Tier 1 market of the United States, signifies a mature yet robust draught beer market in terms of penetration in the on-trade as well as craft beer domination. This is trailed by the Tier 2 market of Mexico, which is primarily driven by the casual dining occasion. Europe continues to be structurally relevant, and Germany and the UK are considered Tier 1 markets, while other markets such as France, Spain, and Italy are Tier 2 markets in which the growth of draft beer is driven by tourism and premiumization trends. The Asia Pacific is the fastest-growing region, whose markets such as Japan and Australia & New Zealand have already established a pattern of beer consumption, hence being considered Tier 1 markets. China, India, and South Korea represent Tier 2 markets and therefore continue to realize growth driven by urbanization and rising incomes, coupled with changing social habits regarding drinking. South America’s leadership in the region under the Tier 1 category is in Brazil, fueled by an extensive bar culture, whereas Argentina & the remainder of the region are in Tier 2 for steady growth prospects. Middle East & Africa’s leadership in the region under the Tier 1 category as hubs in this region are the UAE & South Africa, while Saudi Arabia & the remainder of MEA are in Tier 2.

To learn more about this report, Download Free Sample Report

Recent Development News

- September 2025, HEINEKEN t announced that it has installed a Heineken draught in its 10,000th outlet in Europe. This milestone marks the leadership of the company in the non-alcoholic beer category and underlines mainstream acceptance of alcohol-free options in bars and restaurants across key markets including the Netherlands, UK, Spain, Ireland, and France.

- In September 2025, Draft beer has seen its sales share grow within US foodservice establishments such as bars and restaurants over the past year, and is projected to soon surpass packaged beer sales in value based on a comprehensive research carried out by CGA by NIQ and Draftline Technologies.

|

Report Metrics |

Details |

|

Market size value in 2025 |

USD 12.2 Billion |

|

Market size value in 2026 |

USD 13.5 Billion |

|

Revenue forecast in 2033 |

USD 21.4 Billion |

|

Growth rate |

CAGR of 6.80% from 2026 to 2033 |

|

Base year |

2025 |

|

Historical data |

2021 – 2024 |

|

Forecast period |

2026 – 2033 |

|

Report coverage |

Revenue forecast, competitive landscape, growth factors, and trends |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

United States; Canada; Mexico; United Kingdom; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; United Arab Emirates |

|

Key company profiled |

Anheuser-Busch InBev SA/NV, Heineken N.V., Carlsberg Group, Molson Coors Beverage Company, Asahi Group Holdings, Ltd.,Diageo plc, Kirin Holdings Company, Limited, Sapporo Holdings Limited, Constellation Brands, Inc., Grupo Modelo (AB InBev subsidiary), Tsingtao Brewery Group Co., Ltd., San Miguel Corporation, United Breweries Group, China Resources Beer (Holdings) Company Limited, Boston Beer Company, Inc. |

|

Customization scope |

Free report customization (country, regional & segment scope). Avail customized purchase options to meet your exact research needs. |

|

Report Segmentation |

By Type (Keg Beer, Cask Beer), By Category (Super Premium, Premium, Regular), By End Use (Commercial Use, Home Use) |

Key Draught Beer Company Insights

Anheuser-Busch InBev SA/NV dominates the global draught beer market given the extraordinary breadth of its portfolio, extensive keg distribution infrastructure, and entrenching on-trade partnerships. The company utilizes global flagship brands in concert with regional offerings to satisfy varied consumer tastes and preferences. Scale allows the company to generate cost efficiencies in keg logistics, cold-chain management, and tap system integration, driving deeper relationships with hospitality operators. Meanwhile, AB InBev's aggressive premiumization strategy and investments in craft-style draught brands underpin margin expansion, while its presence in both developed and emerging markets supports stable demand and sustained leadership.

Key Draught Beer Companies:

- Anheuser-Busch InBev SA/NV

- Heineken N.V.

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings, Ltd.

- Diageo plc

- Kirin Holdings Company, Limited

- Sapporo Holdings Limited

- Constellation Brands, Inc.

- Grupo Modelo (AB InBev subsidiary)

- Tsingtao Brewery Group Co., Ltd.

- San Miguel Corporation

- United Breweries Group

- China Resources Beer (Holdings) Company Limited

- Boston Beer Company, Inc.

Global Draught Beer Market Report Segmentation

By Type

- Keg Beer

- Cask Beer

By Category

- Super Premium

- Premium

- Regular

By End Use

- Commercial Use

- Home Use

Regional Outlook

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- Japan

- China

- Australia & New Zealand

- South Korea

- India

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions

Find quick answers to common questions.

The approximate Draught Beer market size for the Market will be USD 21.4 billion in 2033.

Key segments for the Draught Beer Market By Type (Keg Beer, Cask Beer), By Category (Super Premium, Premium, Regular), By End Use (Commercial Use, Home Use).

Major Draught Beer Market players are Anheuser-Busch InBev SA/NV, Heineken N.V., Carlsberg Group, Molson Coors Beverage Company, Asahi Group Holdings, Ltd.

The North America region is leading the Draught Beer Market.

The CAGR of the Draught Beer Market is 6.80%.

- Anheuser-Busch InBev SA/NV

- Heineken N.V.

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings, Ltd.

- Diageo plc

- Kirin Holdings Company, Limited

- Sapporo Holdings Limited

- Constellation Brands, Inc.

- Grupo Modelo (AB InBev subsidiary)

- Tsingtao Brewery Group Co., Ltd.

- San Miguel Corporation

- United Breweries Group

- China Resources Beer (Holdings) Company Limited

- Boston Beer Company, Inc.

Recently Published Reports

-

Dec 2024

Baby Infant Formula Market

Baby Infant Formula Market Size, Share & Analysis Report By ype (Infant Milk, Follow On Milk, Specialty Baby Milk, Growing-Up Milk), By Ingredient (Carbohydrate, Fat, Protein, Minerals, Vitamins, and Others), By Product Form (Powder, Liquid, and Ready-to-feed), By Distribution Channels (Supermarket/Hypermarket, Specialty Store, Pharmacies, Online Retail, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Jan 2025

Edible Insects for Animal Feed Market

Edible Insects for Animal Feed Market Size, Share & Analysis Report By Type (Insect Powder, Insect Meal, Insect Bar, Insect Paste, Insect Oil, and Others), By Insect Type (Beetles, Cricket, Caterpillar, Hymenoptera, Orthoptera, Tree Bugs, and Others), By Application (Livestock, Pet Food, and Aquaculture), By Livestock Type (Poultry, Swine, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Jan 2025

Food Industry Disinfection and Bacterial Control Market

Food Industry Disinfection and Bacterial Control Market Size, Share & Analysis Report By Type (Chemical Disinfectants, Physical Disinfectants, and Biocides and Antimicrobials), By Application (Food Processing Equipment Surface Disinfection, Food Preparation Areas Surface Disinfection, Storage Areas Surface Disinfection, Anti-microbial Coatings Food Preservation, and Preservative Solutions Food Preservation), By End User (Meat and Poultry Processing, Dairy Processing, Seafood Processing, Bakery and Confectionery, Restaurants and Commercial Kitchens, and Food Service Providers), By Sales Channel (Online, Offline), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Jan 2025

Freeze Dried Food Market

Freeze Dried Food Market Size, Share & Analysis Report By Product Type (Fruits, Vegetables, Freeze-Dried Dairy Products, Freeze-Dried Meat and Seafood, Freeze-Dried Pet Food, and Prepared Meal), By Nature (Organic, and Conventional), By Form (Powdered, Granules, and Diced), By End Use (Breakfast Cereals, Dairy Products, Bakery & Confectionery, Nutritional Bars & Supplements, Powdered Beverages, Snacks, and Retail (Household)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031