Market Summary

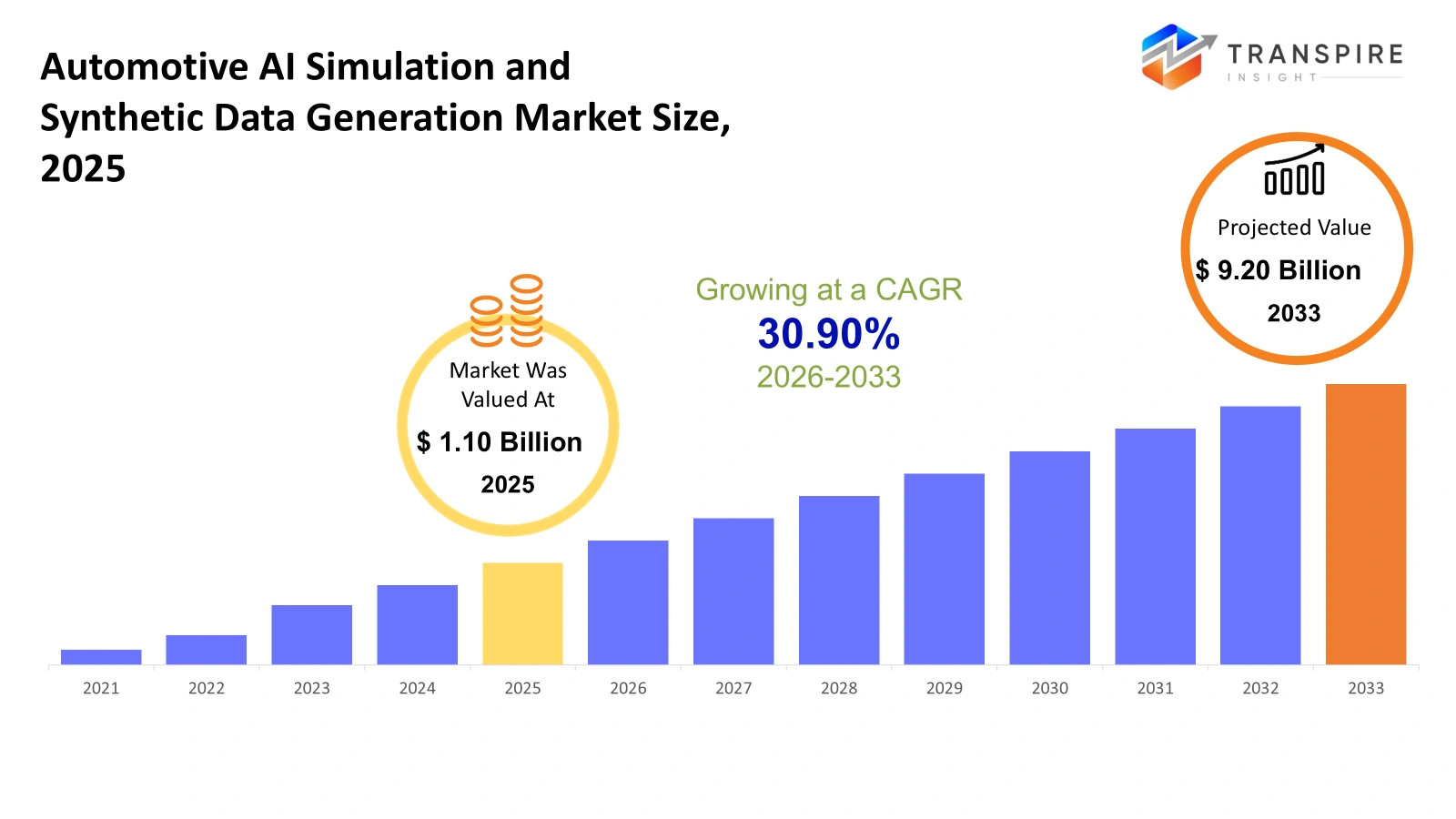

The global Automotive AI Simulation and Synthetic Data Generation market size was valued at USD 1.10 billion in 2025 and is projected to reach USD 9.20 billion by 2033, growing at a CAGR of 30.90% from 2026 to 2033. Fast expansion hits the car-focused AI simulation and fake data scene because self-driving tech plus ADAS keep advancing, needing tons of precise training details for reliable results. Instead of long, expensive road trials, vehicle makers now run checks through digital worlds that mimic real conditions closely. These made-up scenarios help fine-tune smart systems without ever turning an engine on. Testing unfolds inside computers where weather, traffic, and edge cases morph at will. Real streets are not replaced just backed up by endless virtual miles. Performance sharpens faster when limits can be pushed risk-free behind screens.

Market Size & Forecast

- 2025 Market Size: USD 1.10 Billion

- 2033 Projected Market Size: USD 9.20 Billion

- CAGR (2026-2033): 30.90%

- North America: Largest Market in 2026

- Asia Pacific: Fastest Growing Market

To learn more about this report,  Download Free Sample Report

Download Free Sample Report

Key Market Trends Analysis

- The North American market share is estimated to be approximately 42% in 2026. From behind the wheel, North America leads the pack in Automotive AI Simulation and synthetic data creation. Strong roots here come from makers pushing self-driving tech forward. Big names in artificial intelligence add fuel to that engine. Testing vehicles through simulated environments gets serious backing. Money flows into building digital worlds where cars learn before hitting the roads.

- Fueled by big names in auto tech, America holds the top spot. Its edge comes from serious muscle in artificial intelligence studies. Speedy uptake of self-driving tools helps too. Simulation systems catch on fast here, adding momentum.

- Not stopping its climb, Asia Pacific surges ahead thanks to booming car production across the region. New funding pours into self-driving tech, fueling progress step by step. Meanwhile, nations like China, Japan, and South Korea embrace artificial intelligence for testing vehicles in digital environments. Growth ticks upward as these tools become routine in development cycles.

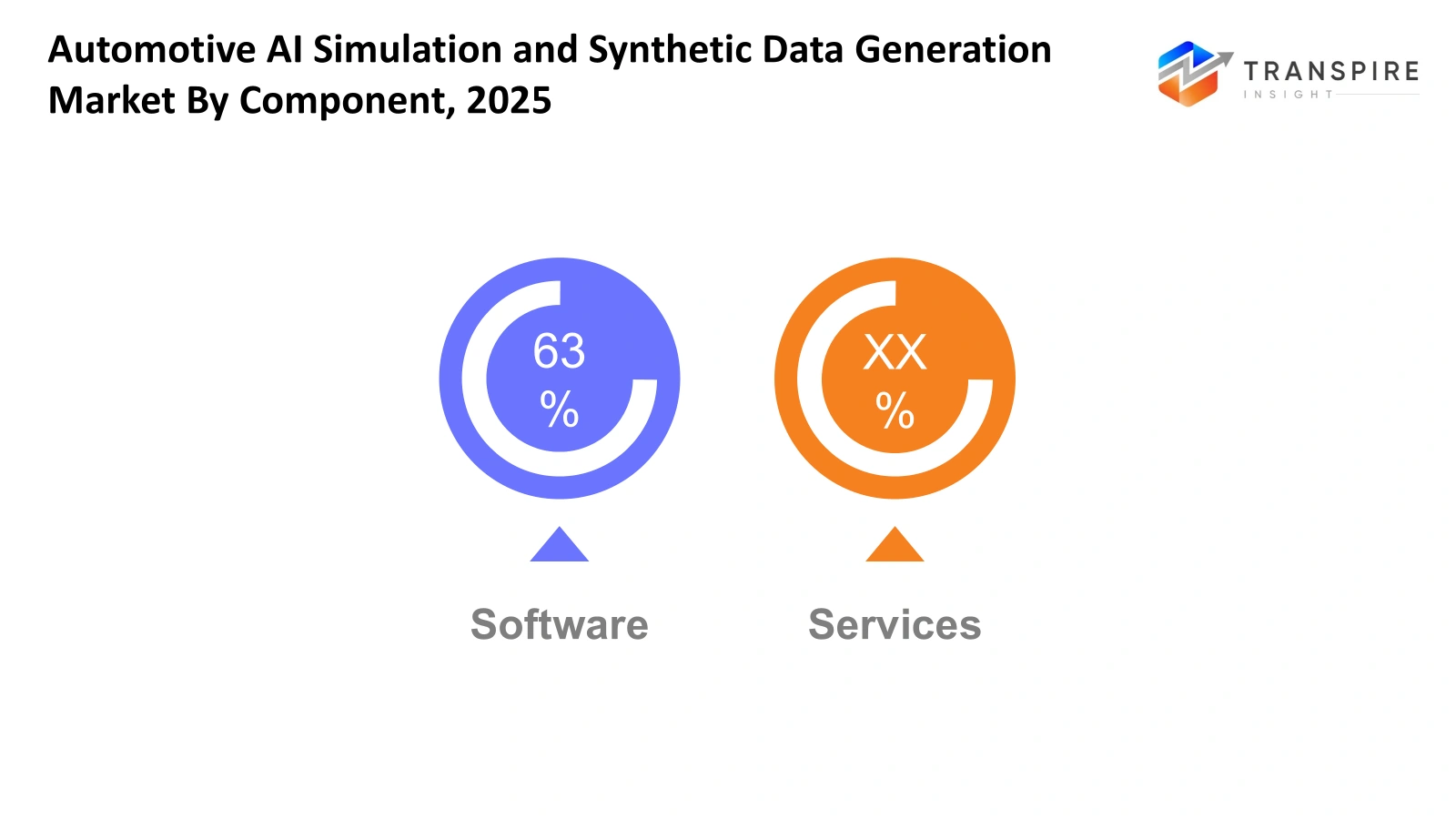

- Software shares approximately 65% in 2026. Software handles AI simulations, tests endless driving situations, shaping fake but realistic data. All of it feeds into building self-driving cars that actually work. Without these tools, progress stalls before hitting the road.

- Out in the open, cloud setups dominate because they grow as needed. Power comes fast when demands spike. These systems handle massive AI workouts without slowing down. Efficiency kicks in where heavy lifting happens across virtual spaces.

- Out in front, simulation platforms take the lead by offering full-scale digital spaces where self-driving tech can be checked without risk. These setups let developers try out scenarios that would be tough to replicate on real roads. Safety comes first here, since mistakes happen in code, not traffic. Efficiency follows because tests run faster when there is no need to wait for weather or road conditions. With everything under control, engineers tweak responses until performance improves. Virtual worlds adapt quickly, making them ideal for repeated trials.

- Big car makers lead here. Their spending on self-driving tech keeps rising. Simulation tools now speed up how fast AI gets tested. Demand for these systems is climbing steadily.

Heavy growth hits the Automotive AI Simulation and Synthetic Data Generation market, fueled by wider use of artificial intelligence inside self-driving cars and smart safety tech like ADAS. Real roads can not supply enough test material fast enough, nor cheaply enough, to train these systems properly. Out of that gap step digital worlds built by machines: flexible setups where lifelike traffic scenarios play out without leaving the lab. Testing speed jumps when software learns from made-up but believable situations at scale, cutting delays across vehicle brain development.

Beginning down new roads, the industry gains ground as car software grows more tangled. Not just that, a shift to vehicles run by code pushes things forward. Car makers, along with tech firms, now lean heavily on simulated environments, which help shape artificial intelligence, check how machines see surroundings, and even measure how well cars handle tricky moments. Better vision systems emerge when digital data throws endless weather, lighting, and edge cases at algorithms. Safety climbs. So does how smoothly everything runs.

Outside of that, better artificial intelligence tools help simulation systems work faster and smarter. Instead of waiting weeks, teams can now generate realistic test data on demand through machine learning methods. Cloud networks support this shift by offering flexible power exactly when needed during complex runs. Digital twins play a role, too. Mirroring actual cars inside virtual worlds gives engineers clearer feedback loops. With these setups, updates happen more often without physical prototypes slowing things down.

More money is flowing in from car makers, tech firms, and self-driving specialists - pushing new ideas forward while speeding up expansion. Development efforts now center on high-level simulators that help refine how driverless systems operate, boost reliability, yet still follow strict safety rules. With vehicles shifting faster into automated, electric, and networked forms, artificial intelligence-driven testing environments plus computer-made scenarios are turning critical one step at a time for building cars that work well, stay secure, and scale smoothly.

Segmentation

By Component

- Software

That's where software steps in. Different models are tested through virtual environments. Training AI becomes faster when fake data is built on demand. Validation checks happen without waiting for real-world inputs. Automotive firms rely on these tools behind the scenes.

- Services

A sudden need arises when setting up simulation tools, and help arrives through guidance on setup, adjustments, connecting systems, plus ongoing updates. Smooth operation stays a priority, while small upgrades happen over time without pause.

To learn more about this report, Download Free Sample Report

By Deployment Mode

- Cloud-Based

Running on remote servers, it adjusts easily to workload changes while delivering instant simulation results. Instead of owning physical hardware, companies tap into vast digital spaces where generating massive datasets becomes affordable. These online systems support dynamic processing needs without upfront investments. Through internet connections, users reach powerful tools that build complex scenarios quickly. Flexibility grows because resources expand or shrink based on demand. Access happens from anywhere, removing location barriers. Performance stays consistent even during peak usage times.

- On-Premises

A building full of servers sits behind a company's own walls, guarded closely. That setup gives teams deeper oversight, tailored configurations, tucked-away information. Some businesses need that locked-down feel when rules demand a tight grip on where data lives.

By Technology

- Simulation Platform

Testing self-driving tech happens inside computer models that copy everyday road situations. These digital spaces let engineers check performance without physical risk. A simulated world runs experiments where cars react to traffic, weather, or pedestrians. Safety improves because mistakes stay within software bounds. Realistic conditions emerge from coded environments built to challenge vehicle responses. Virtual roads allow repeated trials under nearly any condition imaginable.

- Synthetic Data Generation

Out of thin air, fake numbers come alive, crafted to feel true, helping machines learn without needing constant grabs from actual life records. These made-up sets act like mirrors, boosting smarts in software while cutting down hunts for physical facts.

- Digital Twin Technology

Imagine a digital copy of a car, alive inside computers. This mirror version lives alongside real vehicles, moving when they move. Sensors feed live details from actual roads into the system. Engineers watch how each part behaves under stress. Problems show up before breakdowns happen. Testing happens in simulation, saving time on physical trials. Adjustments improve speed, safety, and efficiency together. Changes proven virtually apply directly to the real machine. The environment around it gets modeled too - weather, traffic, terrain. What works digitally stands a better chance in reality.

- AI-Based Scenario Generation

Driving situations unfold through artificial intelligence, building wide-ranging tests without manual input. These generated conditions sharpen how machines learn. Outcomes grow more dependable when systems face unpredictable cases. Complexity emerges naturally during simulation runs. Training gains depth because variations appear frequently. Scenarios differ each time, avoiding repetition. Machine responses adapt as inputs shift unexpectedly.

By End-Users

- Automotive OEM

Picture car makers turning digital tools into driving brains. They run fake road scenarios inside computers before any real tires spin. Instead of waiting for rare crashes, they create them on screens. Think of it like rehearsal tracks for self-driving logic. These tests check how smart cars react when things go sideways. With endless virtual miles logged, safety gets shaped long before launch. Real streets come later - first comes code, sensors, and imagined storms.

- Tier 1 Suppliers

From the start, big auto parts makers use tech tools to test pieces like sensors and smart software ahead of putting them into cars. These companies shape each part carefully, checking how it works long before anything hits the road.

- Technology Companies

Fueled by fresh ideas, tech firms build simulators that mimic real roads. These digital environments help self-driving systems learn without leaving the lab. Instead of waiting for rare events on actual highways, engineers generate scenarios using artificial intelligence. Through clever algorithms, they produce lifelike data where vehicles practice complex decisions. Some teams focus on refining how machines interpret surroundings through sensors. Others improve responses when conditions shift suddenly, like fog rolling in or a pedestrian stepping forward. Each breakthrough adds up, quietly pushing autonomy closer to everyday reality.

- Autonomous Vehicle Developers

Driving software creators turn to computer-made scenarios, since these speed up progress while boosting reliability, without the need for endless road trials. Testing virtual cars in fake environments lets engineers tweak performance safely, avoiding risky outdoor experiments too often. Instead of waiting weeks for physical results, teams study digital outcomes overnight through repeated simulations. Safety checks grow sharper when unusual crash cases are modeled out without harming anyone. Real streets stay less crowded with test vehicles because most learning happens inside machines first.

Regional Insights

Top self-driving car builders are based there. Homegrown automakers team up with tech firms pushing artificial intelligence tools. Think labs filled with digital test tracks instead of asphalt. Big money flows into these virtual proving grounds every year. Safety matters more now than ever before. Companies want fewer crashes during trials. That shift nudges them toward simulated runs and computer-made scenarios. Less time on the roads cuts expenses, too. Watching pixels mimic traffic beats fueling fleets just to gather data. Progress hides inside algorithms trained on fake yet realistic conditions. Real streets still matter, but screens do heavy lifting first.

A major force behind Europe’s role comes from big car makers based there, along with strict rules focused on safer cars and progress in self-driving tech. In nations like Germany, the United Kingdom, and France, spending goes toward using artificial intelligence in simulating tests that speed up how fast driverless vehicles get checked and approved. On top of that, public funding for smarter transport systems, battery-powered cars, and digital advances pushes automakers to rely more on simulated environments and computer-generated scenarios - helping them boost efficiency while meeting safety benchmarks.

Fastest gains should appear across Asia Pacific, fueled by a surging auto sector along with heavy spending on self-driving research in nations like China, Japan, South Korea, and India. Car makers plus tech firms there now turn to artificial intelligence simulations, speeding up design while trimming expenses. Growth creeps forward in Latin America and parts of the Middle East and Africa, lifted by wider use of smart car systems, better digital networks, and rising curiosity around connected transport ideas.

To learn more about this report, Download Free Sample Report

Recent Development News

- June 11, 2025 – NVIDIA releases new AI models and developer tools to the advanced autonomous vehicle ecosystem.

- May 17, 2023 – Parallel domain unveils Reactor, a generative AI-based synthetic data generation engine.

|

Report Metrics |

Details |

|

Market size value in 2025 |

USD 1.10 Billion |

|

Market size value in 2026 |

USD 1.40 Billion |

|

Revenue forecast in 2033 |

USD 9.20 Billion |

|

Growth rate |

CAGR of 3.90% from 2026 to 2033 |

|

Base year |

2025 |

|

Historical data |

2021 – 2024 |

|

Forecast period |

2026 – 2033 |

|

Report coverage |

Revenue forecast, competitive landscape, growth factors, and trends |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

|

Country scope |

United States; Canada; Mexico; United Kingdom; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; United Arab Emirates |

|

Key company profiled |

NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet Inc., Amazon Web Services Inc., Ansys Inc., Siemens AG, dSPACE GmbH, Cognata Ltd., Applied Intuition Inc., Foretellix Ltd., MSC Software Corporation, Altair Engineering Inc., Dassault Systèmes SE, Hexagon AB, MathWorks Inc., and Synopsys Inc |

|

Customization scope |

Free report customization (country, regional & segment scope). Avail customized purchase options to meet your exact research needs. |

|

Report Segmentation |

By Component (Software, Services), By Deployment Mode (Cloud-Based, On-Premises), By Technology (Simulation Platforms, Synthetic Data Generation, Digital Twin Technology, AI-Based Scenario Generation), By End-Users (Automotive OEMs, Tier1 Suppliers, Technology Companies, Autonomous Vehicle Developers) |

Key Company Insights

One key name in Automotive AI Simulation stands out - NVIDIA Corporation. Real power comes from its mix of smart machines and clever code built for self-driving cars. Instead of just parts, it delivers full systems that think on their feet using artificial intelligence. It handles sight, choices, and responses all at once, live. A tool called Omniverse builds fake roads, weather, and traffic so car brains can learn without leaving the lab. Factories shaping tomorrow's vehicles rely on these digital worlds to test how well driverless tech behaves. Partnerships stretch wide: big car builders, part makers, innovators across sectors link up with NVIDIA. Together, they move faster toward smarter transport by simulating dangers before real tires hit pavement. Safety improves when crashes happen only in computers. Speed grows because trials run nonstop inside circuits instead of open lanes.

Key Companies:

- NVIDIA Corporation

- Microsoft Corporation

- Intel Corporation

- Alphabet Inc.

- Amazon Web Services Inc.

- Ansys Inc.

- Siemens AG

- dSPACE GmbH

- Cognata Ltd.

- Applied Intuition Inc.

- Foretellix Ltd.

- MSC Software Corporation

- Altair Engineering Inc.

- Dassault Systèmes SE

- Hexagon AB

- MathWorks Inc.

- Synopsys Inc

Global Automotive AI Simulation and Synthetic Data Generation Market Report Segmentation

By Component

- Software

- Services

By Deployment Mode

- Cloud-Based

- On-Premises

By Technology

- Simulation Platforms

- Synthetic Data Generation

- Digital Twin Technology

- AI-Based Scenario Generation

By End-Users

- Automotive OEMs

- Tier1 Suppliers

- Technology Companies

- Autonomous Vehicle Developers

Regional Outlook

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- Japan

- China

- Australia & New Zealand

- South Korea

- India

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions

Find quick answers to common questions.

The approximate Automotive AI Simulation and Synthetic Data Generation Market size for the market will be USD 9.20 billion in 2033.

Key segments for the Automotive AI Simulation and Synthetic Data Generation Market are By Component (Software, Services), By Deployment Mode (Cloud-Based, On-Premises), By Technology (Simulation Platforms, Synthetic Data Generation, Digital Twin Technology, AI-Based Scenario Generation), By End-Users (Automotive OEMs, Tier1 Suppliers, Technology Companies, Autonomous Vehicle Developers).

Major Automotive AI Simulation and Synthetic Data Generation Market players are NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet Inc., and Amazon Web Services Inc.

The North America region is leading the Automotive AI Simulation and Synthetic Data Generation Market.

The Automotive AI Simulation and Synthetic Data Generation Market CAGR is 30.90%.

- NVIDIA Corporation

- Microsoft Corporation

- Intel Corporation

- Alphabet Inc.

- Amazon Web Services Inc.

- Ansys Inc.

- Siemens AG

- dSPACE GmbH

- Cognata Ltd.

- Applied Intuition Inc.

- Foretellix Ltd.

- MSC Software Corporation

- Altair Engineering Inc.

- Dassault Systèmes SE

- Hexagon AB

- MathWorks Inc.

- Synopsys Inc

Recently Published Reports

-

Dec 2024

3D Optical Profiler Market

3D Optical Profiler Market Size, Share & Analysis Report By Type (Desktop 3D Optical Profiler, and Portable 3D Optical Profiler), By Technology (Confocal Technology, and White Light Interference), By End-Use Industry (Manufacturing, Research Institutions, Automotive, Aerospace and Defense, Medical Devices, and Other), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 - 2031

-

Feb 2025

Depth Sensor Market

Depth Sensor Market Size, Share & Analysis Report By Type (Infrared Depth Sensors, Time-of-Flight (ToF) Sensors, Stereo Vision Sensors, Structured Light Sensors, Ultrasonic Depth Sensors), By Application (Automotive, Robotics, Gaming, Consumer Electronics, Industrial Automation, Healthcare, Security & Surveillance, Others), By End Users (Automotive Manufacturers, Consumer Electronics Companies, Healthcare Providers, Industrial Companies, Security Agencies, Gaming Companies, Robotics Companies, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 – 2031

-

Feb 2025

Digital Manufacturing Market

Digital Manufacturing Market Size, Share & Analysis Report By Component (Hardware, Software, and Services), By Technology (Robotics, 3D Printing, Internet of Things (IoT), and Others), By Application (Automotive and Transportation, Aerospace and Defense, Consumer Electronics, Industrial Machinery, and Others), By Process Type (Computer-Based Designing, Computer-Based Simulation, Computer 3D Visualization, Analytics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 – 2031

-

Feb 2025

Digital Visa Services Market

Digital Visa Services Market Size, Share & Analysis Report By Type (Individual Travelers, Group Travelers), By Application (Tourism, Business Travel, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South and Central America), 2021 – 2031